ISLAMABAD: Saudi businessmen have expressed hope for successful collaborations in Pakistan, saying the country’s economic stability and improved regulatory framework had made it an attractive investment destination, following the signing of over two dozen deals between companies from both nations.

The Kingdom’s Investment Minister Khalid bin Abdulaziz Al-Falih visited Pakistan on a three-day visit with a delegation of over 130 members, including representatives from Saudi companies specializing in energy, mining, and minerals, as well as agriculture, business, tourism, industry and manpower.

The delegation on Thursday signed 27 agreements and memorandums of understanding worth more than $2 billion with several Pakistani companies.

“We saw much change in (Pakistan’s business) regulations which have become much softer,” Sultan Al-Mansour, chairman of All Care Medical Group, told Arab News, pointing out that Pakistan was gradually moving toward economic stability. “All that positive news is making Pakistan a good spot for investment.”

In June 2023, Pakistan constituted the Special Investment Facilitation Council, a hybrid civil-military forum, to facilitate foreign businesses, particularly from Gulf countries.

The Saudi investor hoped for successful collaborations, saying his company had signed two deals with Pakistani businesses developing surgical instruments and operating in the pharmaceutical industry.

“Our (Pakistani) partners will be launching a factory in Saudi Arabia in the foreseeable future,” he informed, adding the South Asian state was rich in human resources and knowledge, and constituted a big market.

Al-Mansour said he had collaborated with Hilbro, a Pakistani company that will supply surgical goods to his organization in the kingdom.

Hilbro’s sales and marketing director, Muhammad Bilal Tariq, said his company would initially supply semi-developed products before setting up a manufacturing unit of surgical goods in Saudi Arabia.

“We are planning to build the factory in Riyadh,” he told Arab News.

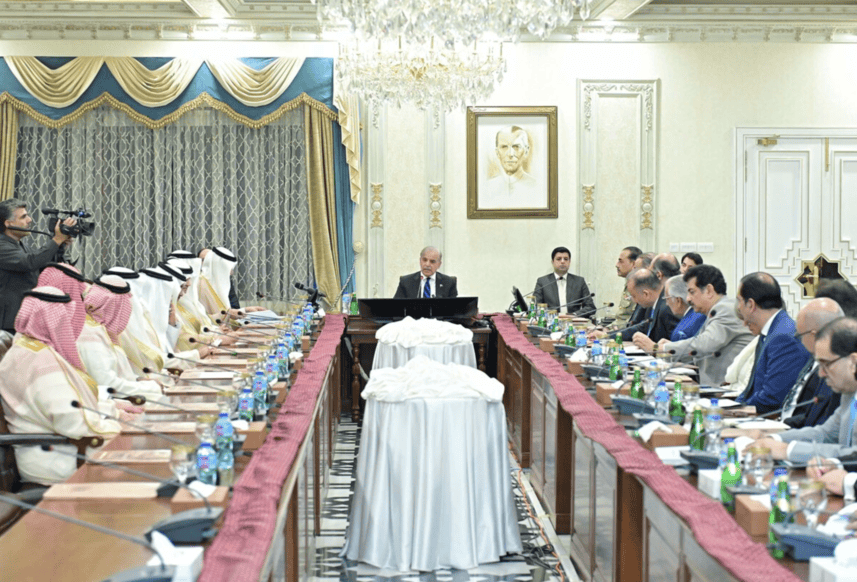

Pakistan Prime Minister Shehbaz Sharif meets Saudi delegation led by Investment Minister Khalid Bin Abdul Aziz Al-Falih in Islamabad on October 10, 2024. (PMO)

Mohammad Al-Madani, CEO of Classera, one of the region’s largest e-learning ed-tech companies operating in over 40 countries, said his organization had supported numerous ministries of education, training institutions and governments globally to transform education and training.

“We have started a big project called eTaleem which aims to transform education using technology across this great nation (of Pakistan),” he said.

He informed that the first phase of operations had already started by partnering with Pakistan Telecommunication Co. Ltd., adding it would use technology to transform education more rapidly and benefit the country’s youth.

“We are talking about 60 million students of Pakistan,” he said.

Al-Madani noted that human capital was a huge asset, pointing out his collaboration in Pakistan would help advance the country.

Mohammad Al-Hijji, chairman of the Saudi investment company Engineering Dimension Holding, said it was a good time to join hands with Pakistani businesses due to the government’s investment-friendly policies.

“It is the right time and we are talking about the investment in our partnership with our brethren at Pakistani renewable energy company Welt Konnect, to invest in a 500-megawatt hybrid power project,” he told Arab News.

His Pakistani partner, Habeel Ahmed Khan, termed the collaboration a “great honor.”

“We signed an MoU with our brothers from ED Holding for the 500-megawatt project that we have been developing in the south of Pakistan, almost 45 minutes east of Karachi in the wind corridor of Gharo,” he said.

Sharing details, he said the project would produce about 168 MW of wind power and 332 MW of solar power.

“It’s going to be one of Pakistan’s first hybrid power projects, which will supply cheap electricity to the national grid,” Khan added.

Ghassan Amodi, CEO of Asyad Holding Group, which is acquiring Shell operations in Pakistan, said the move was part of their strategic plan to expand regionally.

“Our association with Shell is a longstanding relationship, and we look forward to further developing this beyond the borders of Saudi Arabia and now Pakistan. We are also looking for other opportunities,” he said.

Speaking to Arab News, Pakistan’s Petroleum Minister Musadik Malik said over 130 representatives of around 50 Saudi companies were part of the delegation, adding that many projects and collaborations had been finalized in the energy field during the visit.

“Two Saudi companies have flown into Pakistan, and they will be talking about the upgradation of an old refinery, which is about a billion-and-a-half-dollar project,” he said while informing that Pakistan also expected to finish the study on the greenfield refinery project by December.

Pakistan’s Petroleum Minister Musadik Malik speaks during the inauguration of Pak-Saudi Business Forum 2024 in Islamabad on October 10, 2024. (PID)

“Then the conversation will begin to move forward on the $7-10 billion project,” he continued.

Malik informed that once the Saudi delegation departs, the government would follow up on an almost weekly or fortnightly basis.

“It will be to see where those contracts are, how those relationships are evolving and if there’s any government-related trouble that we need to troubleshoot and remove,” he said.