")

RIYADH: Saudi Arabia’s National Debt Management Center has unveiled its Annual Borrowing Plan Report for 2024, outlining the Kingdom’s strategies for financing in the coming year.

The NDMC’s commitment to effective debt management is highlighted by a SR36 billion ($9.6 billion) liability management transaction. This strategic move extended the “Average Time to Maturity,” reducing the risk associated with future maturities.

Speaking to Arab News, economist Talat Hafiz, emphasized that the Kingdom manages the public debt in a “very professional manner that balances between risks and returns on investments.”

He added: “When the Kingdom settles or prepays any debt, it considers a number of factors, among which the future behavior of interest and exchange rates and the realizable cost saving of early retirement of the debt.”

The borrowing plan report sheds light on the achievements of 2023, which provide a solid foundation for the Kingdom as it seeks to sustain fiscal stability and capitalize on opportunities in the upcoming year.

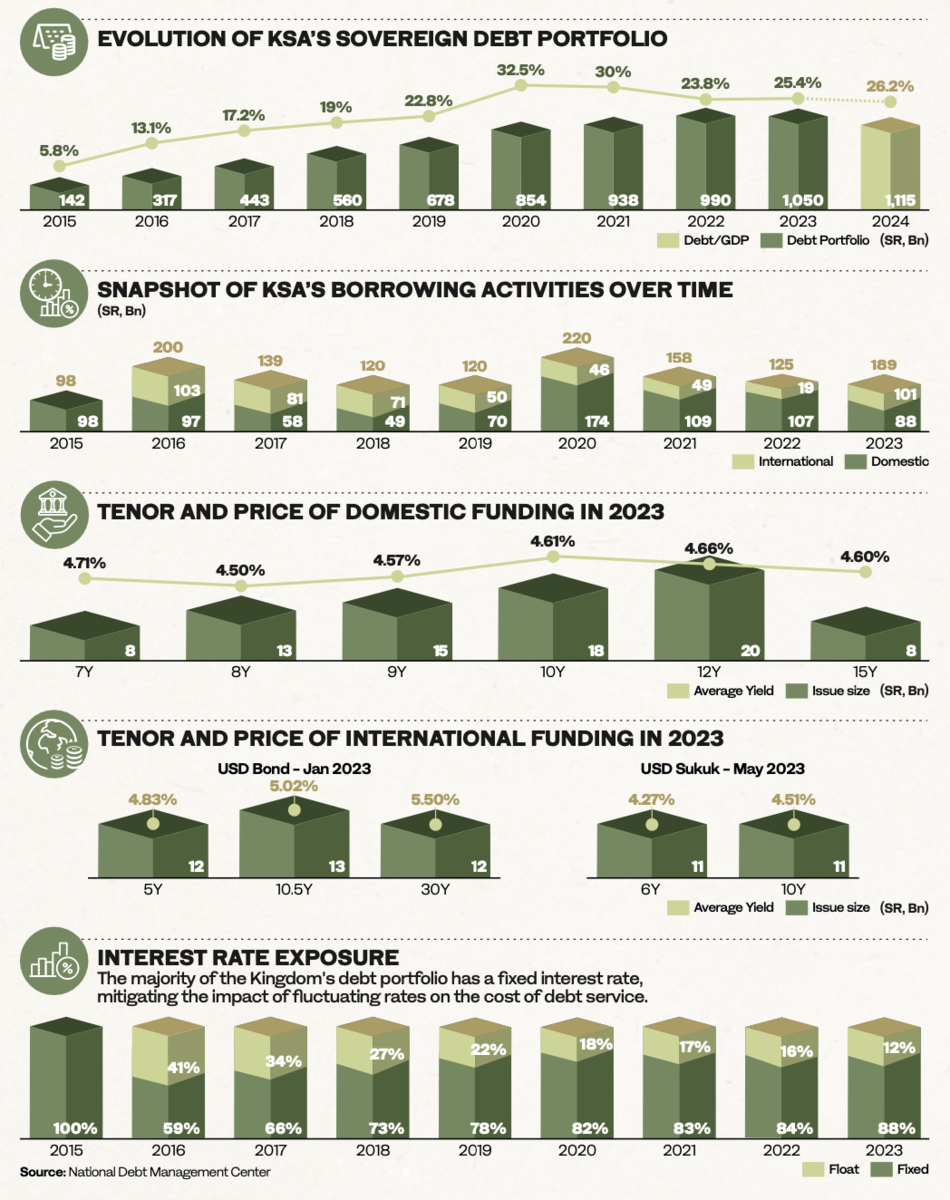

The Kingdom’s debt portfolio exhibited resilience amid rising interest rates, with the “cost of funding” reaching 3.62 percent, and the average time to maturity extending to approximately 9.5 years by the end of 2023.

Balancing debt-raising decisions against key risk factors — liquidity, refinancing, interest rates, foreign exchange, and credit rating — NDMC has ensured a prudent and sustainable debt management strategy.

Overview of 2023: A year of strategic borrowing

The Kingdom witnessed a significant growth of its sovereign debt portfolio in 2023, reaching SR1.05 trillion, equivalent to 25.4 percent of the gross domestic product.

Reflecting on this, Hafiz told Arab News: “The Kingdom is always keen to maintain conservative debt-to-GDP, to avoid loading the Kingdom’s financial system with unnecessary costs of borrowing and also keeping space and room for future borrowing as and when needed.”

He added that Saudi Arabia has set a debt-to-GDP target of 30 percent, which is” very much below world standards of 60 percent.”

The NDMC demonstrated its prowess in debt management by securing SR189 billion in borrowing activities.

Noteworthy was the successful execution of a domestic sukuk and bond liability management transaction, strategically redeeming maturing securities while simultaneously issuing new ones.

In terms of sources, domestic funding contributed 47 percent of the total, showcasing the Kingdom’s resilience.

The remaining 53 percent came from international sources, with oversubscription in the international issuances under the sukuk and global medium-term note program indicating strong investor confidence.

2024 outlook and debt raising guidelines

Building on the success of the 2023 liability management transaction, the Kingdom intends to continue borrowing in 2024, not only to finance the budget deficit but also to refinance debt maturities due in the fiscal year.

The total remaining debt maturities for 2024 stand at SR21 billion, while prefunding activities executed in 2023 secured SR14 billion of the 2024 total financing needs.

The projected budget deficit for 2024 is SR79 billion, resulting in total funding needs of approximately SR86 billion.

By the end of 2024, the total debt portfolio is expected to reach SR1.11 trillion.

Hafiz highlighted that the 2024 Annual Borrowing Plan includes prepayment of SR21 billion debt balance of last year’s borrowing. He also noted that the Kingdom prepaid SR19 billion in 2023.

Investor relations strategy in 2024

A pivotal aspect of the Kingdom’s debt management strategy for 2024 is active engagement with domestic and international investors.

The NDMC aims to foster strong relationships through a comprehensive outreach program that will extend across key regions, including Asia, Europe, and North America.

The center also aims at diversifying the investor base. This move is not only a risk mitigation strategy but also a proactive measure to ensure continued access to global debt markets at favorable rates.

The NDMC seeks to provide investors with the latest updates on the Saudi economy, discuss environmental, social, governance and sustainability initiatives, and showcase the Kingdom’s ambitious Vision 2030 transformation agenda.

Additionally, it plans to extend invitations to international investors to visit the Kingdom.

This engagement will allow investors to interact directly with government leaders and witness the progress of giga-projects that are shaping the nation’s future.

Economic resilience

As the Kingdom continues its journey toward fiscal stability and economic growth, the proactive measures outlined in the report position it to overcome uncertainties in the global financial landscape.

The strategic debt management initiatives, prudent risk management approach, and investor relations strategy underscore the Kingdom’s dedication to maintaining a resilient and sustainable debt profile.

Saudi Arabia’s high credit rating by Fitch, Moody’s, and S&P of ‘A’ with a positive future outlook, has supported the Kingdom’s credit position and enhanced its financial ability and strong commitment not to default on loan payments, according to Hafiz.

He said: “The Kingdom has proven to the world its strong financial portion and its ability to meet its financial obligations before its due.”

By proactively addressing refinancing risks and diversifying the investor base, NDMC aims to ensure Saudi Arabia has continued access to global debt markets and favorable financing conditions.