")

ANKARA: It has been a tumultuous year for Turkey’s economic management with a currency crisis and interest-rate volatility rattling investor confidence.

The recent dismissal of the central bank governor via an overnight presidential decree and the resignation of Berat Albayrak, the Turkish finance minister and son-in-law of President Recep Tayyip Erdogan, contributed to the mood of trepidation.

Now investors are hoping 2021 will bring an improvement to the country’s economic outlook.

Albayrak, who took the finance reins in mid-2018, has been blamed for defending the currency with foreign exchange interventions and depleting foreign reserves of the central bank with costly policy interference in the currency markets.

Turkey is also running a serious current-account deficit — expected to be as much as $2.7 billion in September.

Turkish state banks are reported to have sold about $100 billion in dollar reserves this year to support the currency. Inevitably, such moves by the central bank triggered a rush for dollars among individual depositors seeking a safe haven throughout 2020.

Foreign currency reserves of the country reached their lowest point for the past two decades, resulting in the credit rating agency Moody’s warning in September that Turkey had “almost depleted the buffers that would allow it stave off a potential balance-of-payments crisis.”

As a move to win the trust of investors following the lira’s plunge, the central bank governor was replaced by Naci Agbal and the

finance ministry position was filled by Lutfi Elvan — two close allies of Erdogan. The Turkish lira rebounded against the euro and dollar after the reshuffle of the economy team, however some experts believe this positive direction may be short-lived.

In his first public appearance on Tuesday, Elvan made assurances that the government’s growth policies would not threaten its fight against double-digit inflation that continues to erode the savings of citizens.

“Turkey’s growth process will be planned and controlled in a way that doesn’t contradict our fight for macroeconomic stability and against inflation,” he said, promising that the country would experience a sustainable growth path in two years’ time.

Amid the prospect of early elections and political shakeouts, the economic turmoil is worsening with the currency sinking to record lows as the central bank, under political pressure for not raising rates, held key interest rates steady at around 10.25 percent.

Erdogan is known as a staunch opponent of raising interest rates, branding such monetary policy as “the mother and father of all evil.”

As a critical moment, the central bank will hold its next meeting today to decide on interest rates in a keenly anticipated decision.

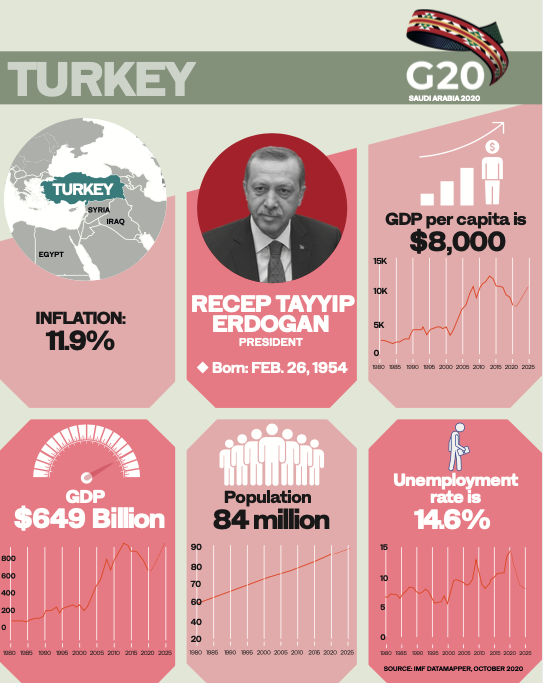

Real rates are considered as much higher than the official figures, with inflation around 12 percent and unemployment rates gradually increasing, especially among youth. More than 10 million people are jobless in Turkey.

The Turkish lira, by far the worst-performing currency, has lost almost 30 percent of its value this year. Under the new Joe Biden administration in the US, the Turkish government may face possible US sanctions over its previous purchase of a Russian missile system.

Wolfango Piccoli, co-president of London-based Teneo Intelligence, said 2020 had shown that Turkey’s model of economic development — largely based on easy credit — was no longer sustainable and was well past its expiry date.

Turkish President Tayyip Erdogan strongly opposes raising interest rates. (AFP)

“Looking ahead, the key question is whether Turkey has officials and politicians able to devise and implement a new economic strategy and whether Erdogan is willing to embrace these changes despite their political cost,” he told Arab News.

With the stakes so high, market watchers expect rate hikes and an end to credit-driven growth of the country that has prevailed for the last three years. The ongoing political pressure on the country’s central bank is also a source of concern for investors.

According to Piccoli — who felt that the new appointments to the economy team did not signal a sudden return to economic orthodoxy — the longer Turkey sticks with the old strategy, the bigger the hole it will find itself in.

As the coronavirus disease (COVID-19) pandemic triggered an annual contraction for the first time in Turkey for more than a decade, Turkey’s economy was this year expected to shrink by 3.4 percent, according to a new Reuters poll. The economy shrank 10 percent in the second quarter.

The last time Turkey’s economy contracted on an annual basis was in 2009, during the financial crisis, when it shrank by 4.7 percent.

Reuters also predicted that the current account balance would post a deficit at around 3.8 percent of gross domestic product this year.

In the meantime, amid the coronavirus outbreak, the latest official figures show Turkey’s tourism income has decreased by more than 70 percent, a slump that has negatively influenced the current account balance.